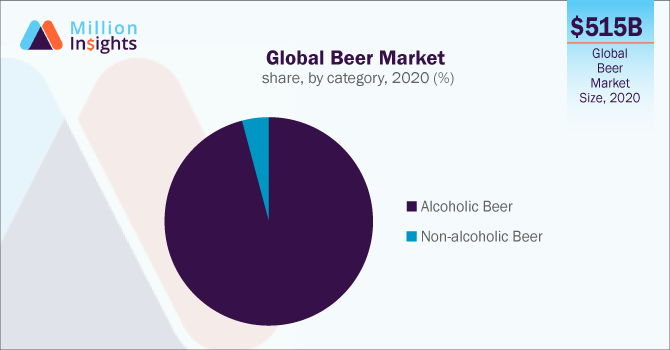

The global beer market size was valued at USD 515.44 billion in 2020 and is expected to expand at a compound annual growth rate (CAGR) of 9.7% from 2021 to 2028. Growing investments by the top players in emerging markets, the introduction of flavored beer, and the increasing number of breweries in developed economies will propel the market growth. Furthermore, changing lifestyles, increasing working population, and the growing popularity of beer among millennials are some of the other factors accelerating the industry growth. Beer is among the most consumed alcoholic beverages in the global market. In addition, consumers’ growing preference for beer over other alcoholic beverages is boosting product sales.

The growing popularity of non-alcoholic beer or low alcoholic beer among health-conscious individuals and those who seek to reduce alcohol consumption will drive the market for non-alcoholic beer in the near future. Top players are significantly investing in non-alcoholic beers to capture a major market share. Anheuser-Busch InBev SA launched a product, Budweiser zero in the non-alcoholic beer category in 2020 and the company has plans to increase its alcohol-free beer production share to 20% by 2025.

Rapid urbanization, increasing consumption of alcoholic drinks, rise in disposable income, and growing adaptability of western culture are positively influencing the market growth at the global level. The availability of beer in various flavors and in the premium category by the top brands further attracts the millennials, thus propelling the market growth.

The imposition of countrywide lockdowns led to the closure of restaurants, pubs, bars, and many places where alcoholic drinks were consumed. During the pandemic, the alcoholic drinks industry witnessed a surge in demand through online retailing where consumers preferred to stay at home and enjoyed drinking at home, which resulted in a grown number of home drinkers. However, as things get normal, it is expected that the reopening of restaurants, pubs, and bars is expected to boost the demand for beer in the near future.

The canned segment accounted for the largest revenue share of over 55.0% in 2020 and is estimated to expand at the fastest CAGR from 2021 to 2028. Off-premise retail channels like supermarkets and hypermarkets are significantly contributing to the segment growth. Consumers increasingly prefer canned beers as they have the ability to maintain the flavor and freshness of beer.

Bottled beer accounted for the second-largest revenue share in 2020. Bottled beer can keep the beer fresh and chilled for a longer period than canned beer. Thus, a large number of consumers prefer to have beer from the bottle only, leading to a grown demand for bottled beer in the global market.

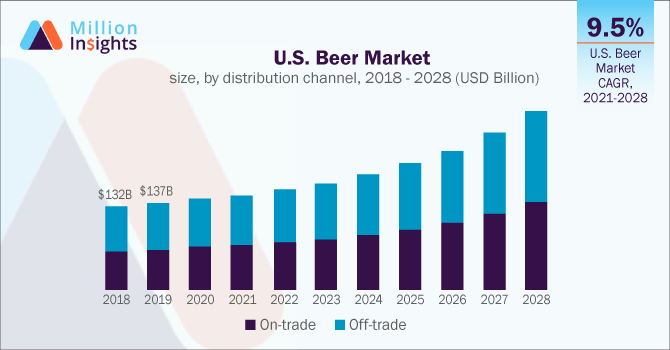

The off-trade segment dominated the market with a revenue share of more than 50.0% in 2020. A large number of consumers are inclined towards home drinking, which is the prime factor for the off-trade segment growth. The availability of beer of various brands at offline channels like supermarkets, retail stores, specialty stores, and conventional stores will drive the market through off-trade channels.

The on-trade channel is expected to expand at the fastest CAGR of 10.1% from 2021 to 2028. The increasing number of pubs, bars, and restaurants across the globe and the growing participation of youngsters at these places will drive the market through on-trade channels in the near future.

Alcoholic beer accounted for the largest revenue share of over 95.0% in 2020 and is estimated to grow at a substantial rate over the forecast period. The rise in popularity and consumption of beer over other alcoholic alternatives will drive the segment. The growing popularity of alcoholic beer in developing countries, the increasing number of microbreweries and brewpubs, and the rising popularity of beer among the young population are fueling the segment growth.

Non-alcoholic beer is expected to expand at the fastest CAGR of 10.3% from 2021 to 2028. The growing trend of low to no alcohol among consumers will drive the segment. The increasing investments by top manufacturers in non-alcoholic brands, the rising demand among health-conscious consumers, and the availability of products in different flavors will further open growth opportunities for the market for non-alcoholic beer in the near future.

North America captured the largest revenue share of over 30.0% in 2020 and will continue to grow at a substantial rate in the forecast period. The rapid expansion of breweries and brewpubs, the availability of local as well as global brands, the growing number of beer consuming individuals, a large chain of pubs and restaurants in this region, and consumers’ willingness to pay for premium brands are some of the key factors responsible for the regional market growth. According to the Brewers Association, the United States had 4,847 breweries in 2015 and the number raised to 8,884 in 2020.

Asia Pacific is estimated to exhibit the fastest CAGR of 10.5% from 2021 to 2028. The rising popularity of beer in developing economies, growing number of restaurants, pubs, and bars across the region, increase in disposable income, the growing participation of the young population in outdoor gatherings, the presence of top brands, and adoption of westernization are some major reasons behind the regional market growth. Countries like China and India are the prime consumers and contributors of beer in this region.

The beer industry is fragmented with the presence of top players holding a majority of the share in the market. Small breweries are strengthening their position by providing unique flavors to consumers. Leading players are expanding their reach across the globe by engaging in mergers and acquisitions, expanding distribution channels, and opening new production facilities. Some prominent players in the global beer market include: -

|

Report Attribute |

Details |

|

Market size value in 2021 |

USD 541.55 billion |

|

Revenue forecast in 2028 |

USD 1038.42 billion |

|

Growth Rate |

CAGR of 9.7% from 2021 to 2028 |

|

Base year for estimation |

2020 |

|

Historical data |

2017 - 2019 |

|

Forecast period |

2021 - 2028 |

|

Quantitative units |

Revenue in USD million/billion and CAGR from 2021 to 2028 |

|

Report coverage |

Revenue forecast, company ranking, competitive landscape, growth factors, and trends |

|

Segments covered |

Category, packaging type, distribution channel, region |

|

Regional scope |

North America; Europe; Asia Pacific; Central & South America; Middle East & Africa |

|

Country scope |

U.S.; Canada; Germany; U.K.; France; Russia; Italy; China; Japan; India; Brazil; Argentina; South Africa; Saudi Arabia |

|

Key companies profiled |

Anheuser-Busch Inbev NV; Heineken N.V.; China Resources Snow Beer Co., Ltd.; Carlsberg; Molson Coors Brewing Company; Tsingtao Brewery Group; Asahi Group Holdings Ltd.; Beijing Yanjing Brewery Co. Ltd.; Kirin Holdings Co. Ltd.; Groupe Castel; Boston Beer Company; Diageo plc; Brewdog plc; Royal Swinkels Family Brewers |

|

Customization scope |

Free report customization (equivalent up to 8 analysts’ working days) with purchase. Addition or alteration to country, regional & segment scope. |

This report forecasts revenue growth at the global, regional, and country levels and provides an analysis of the latest industry trends and opportunities in each of the sub-segments from 2017 to 2028. For the purpose of this study, Million Insights has segmented the global beer market report on the basis of category, packaging type, distribution channel, and region:

Sign up today.

Call us at +1-408-610-2300 to speak with a

representative.