The global luxury cosmetics market size was valued at USD 60.19 billion in 2020 and is expected to expand at a compound annual growth rate (CAGR) of 3.7% from 2021 to 2028. Increasing demand for premium and high-quality cosmetic and personal care products among millennials is driving the market. Additionally, rising demand for a vegan-based cosmetic product is expected to attract consumers toward these products, thereby driving the market. For example, Avon Products Inc., in 2020, launched a cannabis plant-based sativa oil collection, which can be included in various cosmetic products such as creams, cleansers, and body lotions. However, changing fashion trend is likely to drive demand for luxury cosmetic products among fashion professionals and thereby support market growth over the forecast period. Besides, increasing income of the global population and rapid urbanization are other factors fueling the demand for luxury cosmetics.

Luxury cosmetic products are manufactured using premium and high-quality ingredients, which are marketed at a premium price. These products mainly consist of skincare, haircare, makeup, and fragrances. Owing to the high buying power of the consumers, demand for such products is seen increasing from developed regions, such as North America and Europe. However, the demand for luxury cosmetics is also seen rising from developing countries, like India, due to the rising prevalence of skin and hair diseases and increasing disposable income.

The luxury cosmetic industry has been shocked by the COVID-19 crisis. Due to widespread store closures, first-quarter sales have weakened. However, the industry has positively responded to this crisis by switching its brand manufacturing to produce cleaning agents and hand sanitizers. They are also offering free beauty services to frontline workers. The supply chain of various sectors has also been disrupted with the occurrence of the COVID-19 pandemic globally. The impaired distribution network and supply chain are some major challenges that the companies are focusing on. In addition, due to the lockdown, a sales drop was observed in the market.

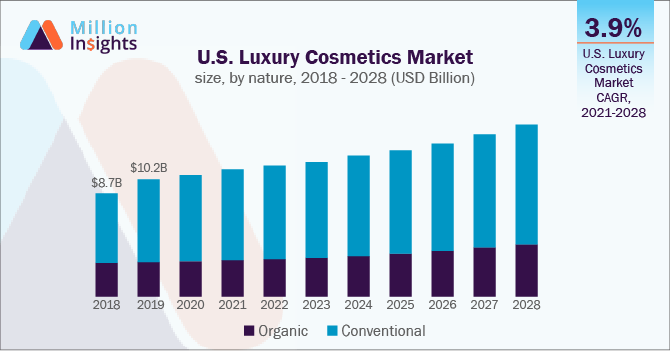

Conventional products accounted for the largest share of over 70.0% in 2020 due to their easy industrial production. They have a longer shelf life as compared to organic products and are economical to produce. Their demand is also increasing from large cosmetic companies, dedicated natural cosmetics companies, contract manufacturers, and formulators and product developers.

The organic cosmetics segment will register the highest growth rate over the forecast period due to the increasing demand from consumers. Many people are becoming health conscious and are focusing on products derived organically and naturally. Organic cosmetics are chemical-free and do not have any side effects as compared to other cosmetic products. Additionally, stringent regulatory policies have forced companies operating in the cosmetic industry to introduce organic products instead of chemical products.

The skincare segment captured the largest share of more than 36.0% in 2020. Owing to the increasing number of brands and transforming business approach, the segment is estimated to witness growth over the forecast period. Furthermore, due to a rise in the health consciousness among individuals and an increase in focus on skincare regimes, the demand for skincare products is expected to increase over the forecast period.

The haircare segment will register the highest growth rate over the forecast owing to its wide usage. The increasing air pollution and growing aging population are the major factors contributing to the increasing demand for hair care products. The growing hair-related problems, coupled with growing trends in the fashion industry, are expected to contribute to the segment growth over the forecast period.

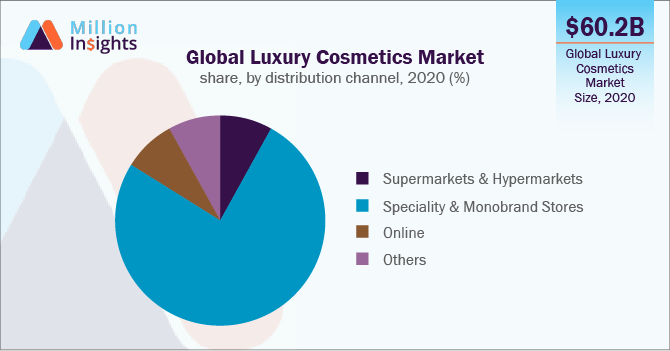

The specialty and monobrand stores held the largest share of more than 75.0% in 2020. Most consumers buying luxury cosmetic products prefer personal service and advice. Specialty and monobrand stores offer personal counseling to customers, hence the preference for these stores is increasing. Due to this reason, this segment is estimated to witness significant growth over the forecast period.

The online channel is estimated to register the fastest CAGR of 4.4% from 2021 to 2028. In addition to the many online luxury cosmetic products, the growing incidence of delivery services and app-based sellers that are significantly popular among consumers is driving the segment. Additionally, exchange or return policy on online platforms attracts the consumers towards more online purchases for luxury cosmetic products.

Europe held the largest share of over 33.0% in 2020 owing to the increasing demand for cosmetics in this region. In addition, the increasing purchasing power of the consumers in this region drives the market. As Europe presents attractive opportunities for the consumer goods sector, the market is projected to witness considerable growth over the forecast period.

Asia Pacific is expected to register the fastest CAGR of 4.7% from 2021 to 2028. This is attributed to the increasing demand for luxury cosmetics in this region. An increase in disposable income in countries, like China and India, is also boosting the market growth in this region. Additionally, the rising expansion of cosmetic companies like Proctor & Gamble Co. in countries like India and China is driving the market in this region.

The main focus of the companies is on innovating new cosmetic products to meet the increasing demand. However, implementing sustainability has its unique limitations and challenges. Various companies are focusing on the expansion and launches of recent developments in the market. For example, in October 2020, Groupe Rocher acquired SabonNYC to expand its cosmetic business in Romania. Some prominent players in the global luxury cosmetics market include: -

|

Report Attribute |

Details |

|

Market size value in 2021 |

USD 62.06 billion |

|

Revenue forecast in 2028 |

USD 80.57 billion |

|

Growth Rate |

CAGR of 3.7% from 2021 to 2028 |

|

Base year for estimation |

2020 |

|

Historical data |

2017 - 2019 |

|

Forecast period |

2021 - 2028 |

|

Quantitative units |

Revenue in USD million/billion and CAGR from 2021 to 2028 |

|

Report coverage |

Revenue forecast, company ranking, competitive landscape, growth factors, and trends |

|

Segments covered |

Nature, product type, distribution channel, region |

|

Regional scope |

North America; Europe; Asia Pacific; Central & South America; Middle East & Africa |

|

Country scope |

U.S.; Germany; U.K.; France; China; Japan; Brazil; South Africa |

|

Key companies profiled |

L'Oréal Group; Shiseido Company Limited; LVMH SE (Christian Dior); Puig SL; Coty, Inc. (JAB Cosmetics B.V.); Oriflame Cosmetics AG; Estee Lauder Companies, Inc.; Revlon, Inc. (MacAndrews & Forbes); Ralph Lauren Corporation; Avon Products, Inc. |

|

Customization scope |

Free report customization (equivalent up to 8 analysts working days) with purchase. Addition or alteration to country, regional & segment scope. |

This report forecasts revenue growth at the global, regional, and country levels and provides an analysis of the latest industry trends and opportunities in each of the sub-segments from 2017 to 2028. For the purpose of this study, Million Insights has segmented the global luxury cosmetics market report on the basis of nature, product type, distribution channel, and region:

Sign up today.

Call us at +1-408-610-2300 to speak with a

representative.