- US: +1-408-610-2300

- Toll Free: +1-866-831-4085

- Become a Client

The China cold chain market size was accounted for USD 10.98 billion in 2016. It is estimated to witness a 10.9% CAGR over the forecasted years, 2017 to 2025. The shifting trend towards the adoption of connected devices and the need for the adoption of warehouse automation, conveyor belts, robots, and truck loading automation is estimated to drive the demand for cold chain solutions.

The need for reducing labor costs, implementing solutions related to workforce forecast and picking optimization is gaining traction across the food processing, pharmaceuticals, and dairy industry. Further, the rising demand for the deployment of workforce management services and solutions is expected to drive the growth of cold chain logistics across China.

The food inspecting and regulatory bodies located across China are imposing several rules and regulations to safeguard and ensure the good quality of food products. They are insisting on cold storage and warehouse operators to provide five temperature zones for food storage. Also, several projects are being undertaken by the Chinese government to widen the supply chain of cold chain products across the country. For example, the governing body has established aquatic products processing & distribution centers for delivering the facility of refrigeration to the pelagic fleets at the Tianjin port.

Several external factors like the widening of retail chains by key organizations, favorable government initiatives, and trade liberalization are anticipated to trigger the market growth for cold chain solutions across China. But, the preference of several consumers residing in urban cities towards the procurement of food products from the wet market is expected to hinder the market growth up to some extent.

The cold chain market can be classified into transportation, monitoring, and storage based on its type. In 2016, the storage segment accounted for the highest share across the market which is further sub-categorized into warehouses and reefer containers. This can be associated with shifting consumer preference over usage of glass and disposable packaging items rather than the conventional plastic ones.

The monitoring segment is expected to register the fastest growth with the highest CAGR in the upcoming years. This can be attributed to the surging need to maintain and monitor several temperature zones as per the requirements. The transportation segment is also expected to gain traction in the upcoming years due to the increasing demand for modern and latest refrigerated vehicles, connected trucks, and trailers for several logistic purposes.

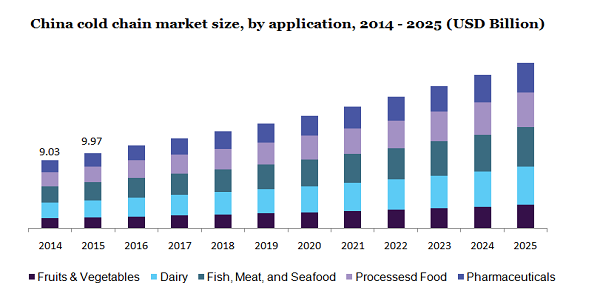

The fish, meat & seafood application segment accounted for the highest share across the China cold chain market in 2016. It is also anticipated to hold a dominant share over the forecasted period, 2017 to 2025. Rising demand for imported food products like Japanese lobsters, Scottish Crabs, Alaskan black cod, and Canadian lobsters coupled with a shifting trend towards adoption of online services of seafood are anticipated to trigger the growth of the cold chain market.

The application segment of processed food is estimated to register significant growth from 2017 to 2025. This can be associated with various factors such as enhanced packaging materials, rapid technological innovation, and its implementation undertaken by the key players.

The industry of cold chain is estimated to witness significant growth in the upcoming years. This can be associated with the rapid technological advances across sectors like the storage, processing, and packaging of seafood. Also, the rising demand for seafood among the millennial population and the surging development of cold chain infrastructure is projected to drive market growth.

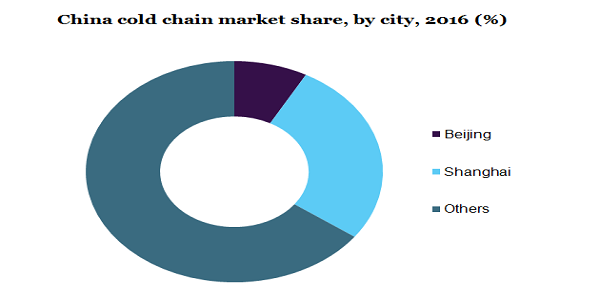

The cold chain market across China has been classified into Shanghai, Beijing, and others (Tianjin, Shenzhen, Guangzhou, and Shandong) based on the region. In 2016, the other segment accounted for the highest share across the market. This can be associated with the increasing number of expos and international exhibitions for launches, promotions, and demonstrations of products related to cold chain and logistics solutions.

The other segment that includes Shandong and the rest of the provinces accounts for a significant share. This can be associated with the procurement of fresh produce across cities like Shanghai and Beijing from Shandong. Further, rising demand for cold storage across this region is expected to trigger up market growth.

The cold chain market across China has been negatively impacted on account of the ongoing COVID pandemic. As this virus originated from Wuhan, the highest numbers of active cases were foreseen across the country in the first quarter of 2020. Also, it has impacted the country’s economic crunch and has brought stagnancy to several operational industries. Moreover, lockdown imposition and restrictions over cargo movement have obstructed the supply chain of processed and cold-stored food items. Further, the reduction in import and export of these perishable food items are expected to hamper the demand for cold chain products in the post-pandemic period.

The key players operating in this market are Swire Group, SF Express, Articold Logistics Ltd., Xianyi Holding Group, Preferred Freezer, and Americold Logistics LLC. They are engaged in implementing technological advances and using IoT solutions for offering enhanced services to their customers.

They are increasing the number of distribution centers, warehouses, cold chain trucks, and logistic support for widening their geographical reach and product portfolio. Further, the rising influence of online channels, chilled and frozen foods is estimated to propel the market growth. Moreover, strategies like partnerships, collaborations, and alliances are being implemented by these players to gain a competitive advantage.

|

Attribute |

Details |

|

The market size value in 2020 |

USD 16.69 billion |

|

The revenue forecast in 2025 |

USD 27.79 billion |

|

Growth Rate |

CAGR of 10.9% from 2017 to 2025 |

|

The base year for estimation |

2016 |

|

Historical data |

2014 - 2015 |

|

Forecast period |

2017 - 2025 |

|

Quantitative units |

Revenue in USD billion and CAGR from 2017 to 2025 |

|

Report coverage |

Revenue forecast, company ranking, competitive landscape, growth factors, and trends |

|

Segments covered |

Type, application, and city. |

|

Country scope |

China (Beijing, Shanghai, Shandong, Tianjin, Shenzhen, Guangzhou, and others) |

|

Key companies profiled |

Swire Group; Articold Logistics Ltd.; Shandong Gaishi International Logistics Group (Gaishi Group); SF Express; and Xianyi Holding Group. |

|

Customization scope |

Free report customization (equivalent up to 8 analysts working days) with purchase. Addition or alteration to country, regional & segment scope. |

|

Pricing and purchase options |

Avail of customized purchase options to meet your exact research needs. |

This report forecasts revenue growth at the country level and provides an analysis of the latest industry trends from 2014 to 2025 in each of the sub-segments. For the purpose of this study, Million Insights has segmented the China cold chain market on the basis of type, application, and city:

• Type Outlook (Revenue, USD Million, 2014 - 2025)

• Storage

• Warehouse

• Bulk Storage

• Production Stores

• Ports

• Refrigerated Containers

• 20 ft.

• 40 ft.

• 48 ft.

• 53 ft.

• Transportation

• Road

• Sea

• Rail

• Air

• Monitoring Components

• Hardware

• Sensors

• RFID Devices

• Telematics

• Networking Devices

• Software

• Application Outlook (Revenue, USD Million, 2014 - 2025)

• Fruits & Vegetables

• Dairy

• Fish, Meat, and Seafood

• Processed Foods

• Pharmaceuticals

• City Outlook (Revenue, USD Million, 2014 - 2025)

• Beijing

• Shanghai

• Other Cities (Shandong, Tianjin, Shenzhen, Guangzhou, and others)

Research Support Specialist, USA