- US: +1-408-610-2300

- Toll Free: +1-866-831-4085

- Become a Client

The global food container market was prized by USD 145.6 billion in 2020. It is estimated to witness a 4.2% CAGR from 2021 to 2028.

The enlargement of the market is likely to be powered by the rising global demand for wrapped-up foodstuff products. Furthermore, the handiness presented by these containers in wrapping, moving, and transportation of the foodstuff products is one of the most important factors, pushing the demand for the product, within the global market.

Principally, packaged foods comprise desserts, cake mixes, RTE convenience foods, snacks, frozen meals, Ready-To-Eat (RTE) meals, plus others. The rising demand for these types of foodstuffs is estimated to push the manufacturing companies to increase production capacity, sequentially, which will stimulate demand for the food containers during the forecast period. The global food container market observed slow expansion in 2020, owing to the Covid-19 pandemic.

Food containers assist in rising the shelf life of the products by means of protecting and avoiding food items from worsening. The rising alertness of the customers about the ecological problems and sustainability is anticipated to affect the market.

Besides, the rising concentration of the manufacturing companies on modernization, in addition to aesthetics of the food containers is, moreover, considerably magnetizing food manufacturing companies to present their products in diverse inventive types. Sequentially, this is estimated to stimulate the expansion of the market, during the nearby future.

The global food container market experienced a slothful increase, in 2020, owing to the eruption of the Covid-19 pandemic. The shortage of raw material, because of the disturbance in the supply chain, caused the abridged manufacture of food containers. A number of most important companies observed a drop in their yearly profits, in 2020. For example, in a contrast to 2019, the yearly proceeds of Amcor plc decreased by roughly 6.0%, in 2020.

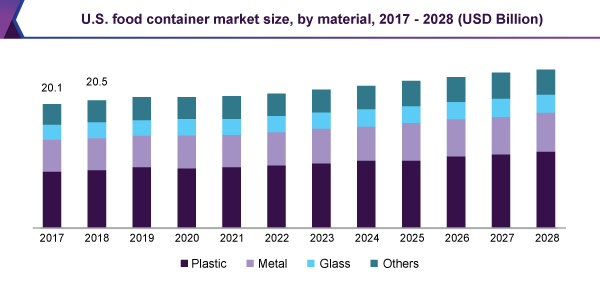

The plastic section held more than 46.0% revenue share and dominated the market, in 2020. Based on the material, the market has been separated into glass, plastic, metal, and others. Because of its numerous advantages above other options, plastic is the most broadly utilized material in the market for packaging. In comparison with other materials, plastic is lighter in weight. In contrast to additional materials, like glass and metals, plastics are fairly low-priced.

In accordance with the American Chemistry Council, merely two pounds of plastic resins are necessary to pack up 10 gallons of drinks. While, about forty pounds of glass, eight pounds of steel, and three pounds of aluminum are necessary to distribute a similar amount of drink. Diverse categories of plastic resins are utilized to manufacture plastic containers, for example, polystyrene, PET, HDPE, PP, and LDPE.

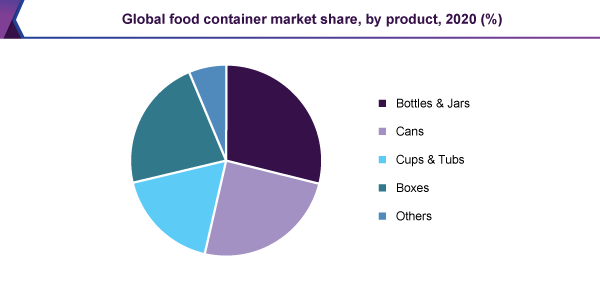

In 2020, the bottles & jars product section held above 28.0% revenue share and dominated the food container market. Generally, these are the extensively utilized goods in the rigid food wrapping section.

The diverse categories of food items are filled in different forms of bottles as well as jars, manufactured using plastics and glass. For example, meat, fish, syrups, oil, mayonnaise, sauces, jams, processed fruits and vegetables, spread, spices, cheese, and honey.

The cans product section is projected to record the highest, above 4.5% CAGR, during the forecast period, owing to the increasing demand for different canned beverages and food items.

Besides, the cups & tubs section is likely to record the major CAGR, during the forecast period. Generally, this can be credited to their particular use for non-viscous and thick foodstuff products. Mainly, the cups & tubs are utilized to pack confectionery, desserts, and bakery, products, for example, cakes, pudding, and ice cream. Glass, as well as plastic, is mainly utilized to produce cups & tubs.

In 2020, Asia Pacific held more than 36.0% revenue share and led the global food container market. It is projected to be the highest rising local market during the forecast period. This progress can be accredited to the fast increasing business of food processing, within the region, owing to the sound support by the government. The nations like Japan, China, and India, are the most important providers to the enlargement of the regional market in the Asia Pacific.

North America is projected to develop by a stable 3.0% CAGR, during the forecast period. The rising demand for convenience, as well as parceled foods between the employed people, can be credited to this enlargement. Growing demand for canned foods, for example, canned meat, and fish, in the U.S.A. is, moreover, speeding up the expansion of the market, within the state. Consistent with the information published by the Delaware Sea Grant, in 2017, roughly 55.0% of the entire seafood used up in the U.S. was restricted to canned shrimp, salmon, and tuna.

Owing to the attendance of local, global and regional manufacturing companies, the market for food container is extremely aggressive. The manufacturing companies present a broad variety of products having diverse formats, shapes, and sizes. The contest between the companies is sourced from various considerations. It includes sustainability, quality, product contributions, recyclability, price, and the reputation of the business.

A number of important policies have been implemented by the majority of companies to make stronger their place in the market and increase their share. These policies include mergers & acquisitions, enlargement of the delivery network, presentation of new products, joint ventures, and modernization.

• Ball Corp.

• Graham Packaging Company, Inc.

• Plastipak Holdings, Inc.

• Ardagh Group

• Amcor plc

• Tetra Pak

• Weener Plastics

• Sonoco Products Company

• Berry Plastics Corp.

• Silgan Holdings, Inc.

|

Report Attribute |

Details |

|

The market size value in 2021 |

USD 147.5 billion |

|

The revenue forecast in 2028 |

USD 201.9 billion |

|

Growth rate |

CAGR of 4.2% from 2021 to 2028 |

|

The base year for estimation |

2020 |

|

Historical data |

2017 - 2019 |

|

Forecast period |

2021 - 2028 |

|

Quantitative units |

Revenue in USD million/billion and CAGR from 2021 to 2028 |

|

Report coverage |

Revenue forecast, company ranking, competitive landscape, growth factors, and trends |

|

Segments covered |

Material, product, region |

|

Regional scope |

North America; Europe; Asia Pacific; Central & South America; Middle East & Africa |

|

Country Scope |

U.S.; Canada; Mexico; Germany; France; U.K.; Italy; China; Japan; India; Australia; Brazil; Argentina; Colombia; Saudi Arabia; UAE; South Africa |

|

Key companies profiled |

Amcor plc; Silgan Holdings, Inc.; Ardagh Group; Berry Plastics Corp.; Plastipak Holdings, Inc.; Sonoco Products Company; Graham Packaging Company, Inc.; Weener Plastics; Ball Corp.; Tetra Pak |

|

Customization scope |

Free report customization (equivalent up to 8 analysts working days) with purchase. Addition or alteration to country, regional & segment scope. |

|

Pricing and purchase options |

Avail of customized purchase options to meet your exact research needs. |

This report forecasts revenue growth at global, regional, and country levels and provides an analysis of the latest industry trends in each of the sub-segments from 2017 to 2028. For the purpose of this study, Million Insights has segmented the global food container market report based on material, product, and region:

• Material Outlook (Revenue, USD Million, 2017 - 2028)

• Plastic

• Metal

• Glass

• Others

• Product Outlook (Revenue, USD Million, 2017 - 2028)

• Bottles & Jars

• Cans

• Cups & Tubs

• Boxes

• Others

• Regional Outlook (Revenue, USD Million, 2017 - 2028)

• North America

• U.S.

• Canada

• Mexico

• Europe

• Germany

• France

• U.K.

• Italy

• The Asia Pacific

• China

• Japan

• India

• Australia

• Central & South America

• Brazil

• Argentina

• Colombia

• Middle East & Africa

• Saudi Arabia

• UAE

• South Africa

Research Support Specialist, USA