- US: +1-408-610-2300

- Toll Free: +1-866-831-4085

- Become a Client

The global 5G chipset market size was accounted for USD 1.1 billion in the year 2019 and projected to grow with a CAGR of 63.4 % over the forecast period, from 2020 to 2027. The rising demand for a high-speed network with less than 1ms latency to offer continuous connectivity is expected to fuel the market growth during the forecast period.

The 5G chipset module is considered an essential component in laptops, smartphones, telecom, and routers. This module allows to access next-generation data networks to enhance the user’s experience.

Various telecom operators across the world including Verizon Communications; AT&T, Inc.; and China Telecom Corporation Limited are increasingly deploying 5G network infrastructure to offer high-speed connectivity to their consumers. For example, in 2018, Nokia Corporation has done an agreement worth nearly 2.2 USD billion with three Chinese telecom players including China Mobile Limited, China United Network Communications Group Co., Ltd., and China Telecom Corporation Limited, to deploy high-speed networks in China. This factor is expected to increase the adoption of 5G network infrastructures across the globe, thereby expected to also drive the 5G chipset module demand in the near future.

Moreover, the rising demand for high-speed connective for drones and Vehicle to Everything is also projected to fuel the market growth during the forecast period Internet of Things(IoT) is gaining popularity across the globe due to the installation of smart grids, smart cities, and smart infrastructure projects. According to Million insight research analysis, the IoT connections are estimated to exceed around 2.5 billion by the end of 2027. Various manufactures are implementing IoT to improve their productivity by monitoring machine and equipment performance in real-time. These above-mentioned factors are expected to raise IoT-based devices which are expected to positively influence the 5G chipset market in the coming years.

Continuous focus to develop innovative chipset modules for the telecom sector to reduce power consumption is projected to open new avenues for market growth. For example, in 2019, Samsung Electronics Co., Ltd. launched a 5G chipset component that is capable to operate within the mmWave band. This component is designed to reduce power consumption weight by 25.0% along with size.

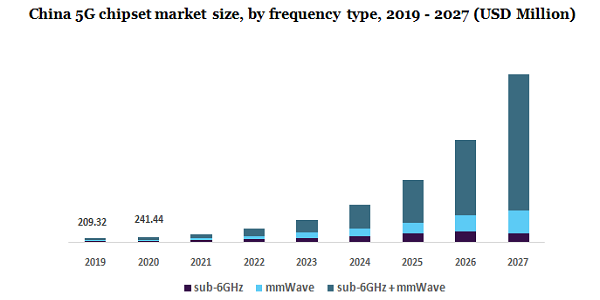

The sub-6GHz frequency type dominated the market, in 2019 and accounted for the largest market share of over 79.0% in terms of revenue. This is due to the initial providing 5G chipset module supports to sub-6GHz by market players for connected cars, smartphones, and laptops. On the basis of frequency type, the market is segmented into sub-6GHz + mmWave, and sub-6GHz, mmWave. The sub-6GHz + mmWaveis projected to have robust growth over the forecast period due to continuous advancement in chipset modules supporting both bands in a single module.

The emergence of the Industrial Internet of Things(IIoT) and the increasing trend of automated cars have generated the need for fast data networks and higher bandwidth. The chipset demand is increasing which is supporting to mmWave band, thereby expected to drive the segment growth. In addition, the growing trend of smart homes along with IoT devices will require high bandwidth and high-speed data in the next few years, which is expected to boost the mmWave segment growth over the forecast period.

In 2019, 7nm processing node dominated the global market and accounted for the largest market share of over 69.0%. The rising focus of key market players to develop 7nm processing nodes is a key factor to drive the segment growth. Major players like Huawei Technologies Co. Ltd.; MediaTek Inc.; Intel Corporation, and Qualcomm Incorporated are focusing to develop this processing node. Moreover, these key players are focusing on the development of 10nm and 7nm processing nodes to support high band frequencies. In developed regions, automated cars are becoming popular, the need to support seamless connectivity among vehicles has grown and processing nodes play an important role to develop 5g chipset modules.

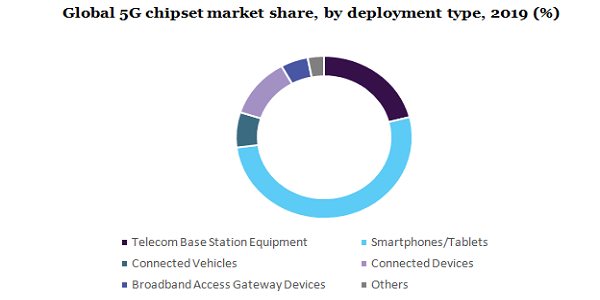

On the basis of deployment, the 5G chipset market is segmented into telecom base station equipment, smartphones/tablets, connected vehicles, connected devices, broadband access gateway devices and others In 2019, the smartphones/tablet segment accounted for the leading market share of around 56.0% in terms of revenue. The high revenue share can be attributed to the increasing demand for 5G enable tablets/smartphones for watching high definition videos, video calling, and online gaming, applications.

5G enabled chipsets to have a huge demand across several devices and equipment such as smartphones, tablets, connected devices, and telecom base station equipment. Moreover, continuous development in next-generation technology is expected to further drive the market growth Hence, the telecom base station equipment deployment type held over 18.0% market share, in 2019. In addition, deployment of 5G technologies in the automotive industry will enable vehicles to connect with the high-speed networks, thereby expected to drive the 5G chipset demand in connected vehicles.

Major market players including Huawei Technologies Co. Ltd., Qualcomm Incorporated, and, Intel Corporation are concentrating on the development of a single 5G chipset module that is capable of supporting non-standalone and standalone carrier frequency. Ensure high-speed connectivity in smart devices being deployed in various industries such as manufacturing, healthcare, and utility is expected to drive the market growth in the near future. These connected devices segment is projected to witness significant growth over the forecast period, 2020 to 2027.

In 2019, the IT& telecom sector held the largest 5G chipset market share of over 34.0%. This is due to high investment by key market players for developing 5G chipset components for broadband gateway devices, telecom base stations, and other communicational devices. Moreover, growing demand for 5G chipset across various end-use industries such as energy & utilities, transportation & logistic, manufacturing, IT & telecom, and others is expected to further propel the product demand. This is fueling the need for high-speed data for corporate applications is also anticipated to fuel the market growth in the IT & telecom sector over the forecast period.

In the manufacturing industry, rising awareness about digitalization among incumbents in order to enhance productivity is projected to drive market growth. Further, the rising need for wireless communication among actuators, sensors, and robots and automation in production lines is expected to exhibit growth of this segment over the forecast period.

In 2019, Asia Pacific accounted for the largest market share of over 46.0%. This high revenue share can be attributed to growing investment in 5G-enabled smart devices as well as base stations that supports new radio frequencies. Further, this region is projected to grow with a 67.1% CAGR over the forecast period. Key players including Huawei Technologies Co. Ltd., and Samsung Electronics Co., Ltd., are investing in the development of the 5G chipset. The rising popularity of smart manufacturing in developing countries like India and China is expected to drive the 5G chipset components to demand over the forecast period.

The U.S. is expected to witness significant growth in the next few years due to high investment in the deployment of smart cities and building smart homes. Additionally, the emergence of smart transportation infrastructure and automated driving cars are expected to surge the market growth in the U.S.

The high spread of COVID-19 across the globe had an adverse impact on 5G chipset manufacturing, which has led to a slowdown in production in several countries such as China, U.S., and South Korea. This scenario has enforced various supply chain contributors to shift their production facilities outside China. Major players such as Samsung Electronics Co., Ltd., and Huawei Technologies Co., Ltd. have slowdown their 5G chipset production. Hence, there will be some delay in the development and up-gradation of 5G-enabled products by telecom network providers.

However, companies like Qualcomm and Broadcom are relatively less affected by the Coronavirus pandemic and continuing their productions to expand their footprints in the market on 5th June 2020, Nokia announced a collaboration with Broadcom to develop advanced semiconductor modules including system-on-chip (SoCs) solutions which will be integrated into Nokia’s 5G-enable product portfolio. This collaboration will also help to expand Nokia’sReefShark chipsets used for 5G solutions to improve system performance

Market players are adopting several market strategies such as collaboration, partnerships, product innovation, and development to strengthen their footprints in this market. In addition, these players are concentrating to develop new products to enhance their product portfolio and to gain maximum market share. For example, Qualcomm Incorporated launched Snapdragon X55 5G modem, in 2019. Further, key players are also investing in R&D to develop multi-mode 5G chipset hardware components. For example, in 2018, Intel Corporation invested USD 28.7 billion in R&D to develop innovative technologies. The company has also done this investment to sustain itself in a competitive market. The key players are operating in this market are as follows:

• MediaTek Inc.

• Infineon Technologies AG

• Qualcomm Incorporated

• Intel Corporation

• Xilinx Inc.

• Qorvo, Inc.

• Huawei Technologies Co. Ltd.

• Samsung Electronics Co., Ltd.

• Unisoc Communications, Inc

|

Attribute |

Details |

|

Market Size Value in 2020 |

USD 1.3 Billion |

|

Revenue Forecast in 2027 |

USD 40.4 Billion |

|

Growth Rate |

CAGR of 63.4% from 2020 to 2027 |

|

The base year for estimation |

2019 |

|

Historical data |

- |

|

Forecast Period |

2020 - 2027 |

|

Quantitative Units |

Revenue in USD Million and CAGR from 2020 to 2027 |

|

Report coverage |

Revenue forecast, company ranking, competitive landscape, growth factors, and trends |

|

Segment Covered |

Frequency type, processing node type, deployment type, vertical, region |

|

Regional scope |

North America; Europe; Asia Pacific; Latin America; MEA |

|

Country scope |

U.S.; Canada; U.K.; Germany; Sweden; China; Japan; India; South Korea; Brazil; Mexico |

|

Key companies profiled |

Qualcomm Incorporated; Intel Corporation; Huawei Technologies Co. Ltd.; Samsung Electronics Co., Ltd.; MediaTek Inc.; Infineon Technologies AG.; Unisoc Communications, Inc.; Xilinx Inc.; and Qorvo, Inc. |

|

Customization Scope |

Free report customization (equivalent up to 8 analyst’s working days) with purchase. Addition or alteration to country, regional & segment scope. |

|

Pricing and Purchase options |

Avail of customized purchase options to meet your exact research needs. |

This report forecasts revenue growth at the global, regional, and country levels and provides an analysis of the latest industry trends in each of the sub-segments from 2019 to 2027. For the purpose of this study, Million Insights has segmented the global 5G chipset market report based on frequency type, processing node type, deployment type, vertical, and region:

• Frequency Type Outlook (Revenue, USD Million, 2019 - 2027)

• sub-6GHz

• mmWave

• sub-6GHz + mmWave

• Processing Node Type Outlook (Revenue, USD Million, 2019 - 2027)

• 7 nm

• 10 nm

• Others

• Deployment Type Outlook (Revenue, USD Million, 2019 - 2027)

• Telecom Base Station Equipment

• Smartphones/Tablets

• Single-Mode

• Standalone

• Non-Standalone

• Multi-Mode

• Connected Vehicles

• Single-Mode

• Standalone

• Non-Standalone

• Multi-Mode

• Connected Devices

• Single-Mode

• Standalone

• Non-Standalone

• Multi-Mode

• Broadband Access Gateway Devices

• Single-Mode

• Standalone

• Non-Standalone

• Multi-Mode

• Others

• Single-Mode

• Standalone

• Non-Standalone

• Multi-Mode

• Vertical Outlook (Revenue, USD Million, 2019 - 2027)

• Manufacturing

• Energy & Utilities

• Media & Entertainment

• IT & Telecom

• Transportation & Logistics

• Healthcare

• Others

• Regional Outlook (Revenue, USD Million, 2019 - 2027)

• North America

• U.S.

• Canada

• Europe

• U.K.

• Germany

• Sweden

• the Asia Pacific

• China

• India

• Japan

• South Korea

• Latin America

• Brazil

• Mexico

• Middle East & Africa

Research Support Specialist, USA