- US: +1-408-610-2300

- Toll Free: +1-866-831-4085

- Become a Client

The global 5G system integration market size was accounted for USD 7.66 billion in 2019. It is predicted to register a CAGR of 23.8% over the forecast duration, 2020 to 2027. 5G system integration is the development of combining both physical and virtual components of enterprise with brand new systems to work over the latest 5G connectivity. The increasing demand for high-speed connectivity has allowed enterprises to implement enhanced networks to improve overall efficiency and lowering overall costs. Thus, the rapid implementation of enhanced networks infrastructure in enterprises to deliver seamless services to the customers is predicted to bode well for market growth over the estimated period.

Leading industry players are utilizing opportunities to supplement their operations by incorporating the latest technologies to boost industry 4.0. These latest technologies, such as wireless cameras, cloud robots, and big data analytics, are permitting producers to get an edge over data-driven operations. Manufacturers are focusing on integrating the latest 5G network, to offer solicited communication to these latest technologies, which assist in lowering operational downtime and cost. Thus, rapid implementation of IoT along with increasing demand for 5G services to offer solicited connectivity is expected to proliferate the 5G systems demand in the upcoming years.

Owing to the growth of the 5G mobile network, several organizations worldwide emphasizing integrating their traditional network with this latest connectivity. This integration will assist companies to leverage high bandwidth with low cost for their operations, which, in turn, will enhance overall productivity. Therefore, the noticeable increase in demand for high-speed broadband to lower the response time is projected to fuel the market growth over the forecast years.

The growing preference for Network Function Visualizations (NFV) and Software-Defined Networking (SDN) is also anticipated to bolster the product demand in the upcoming years. NFV permits companies to implement many firewalls and virtual machines. The SDN offers a smart network infrastructure and assists in managing the application of a company-owned network efficiently. However, the robust rise in data sets stored in the cloud, and surging demand for a cloud-built application, create a security concern in the customers, that may restrain the market growth from 2020 to 2027.

The recent outbreak of COVID-19 has adversely affected the expansion of 5G networks. Countries such as Spain, U.K, France, and the U.S have postponed their spectrum auctions owing to this pandemic. Further, the leading network provides including Ericson, Nokia Corporation, and Huawei have delayed the deployment for 5G networks. Thus, the delay in the setting of the 5G network is affecting the 5G system integration market.

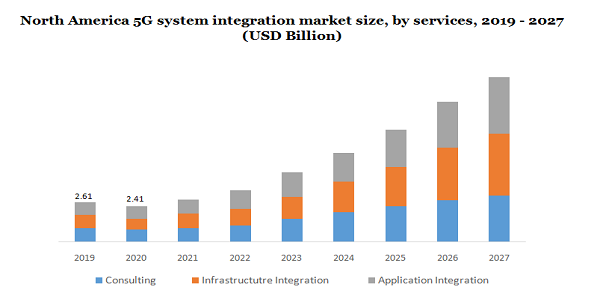

The infrastructure integration division occupied the largest market share of 37.8% in 2019 and ascends with a steady CAGR over the forecast period. Factors such as increasing demand for 5G infrastructure and high-speed broadband are expected to augment the product demand in the upcoming years. The infrastructure services include Data Center Infrastructure Management (DCIM), network integration, and building management among others.

The consulting category is estimated to ascend with a CAGR of 21.1% from 2020 to 2027. The surging demand for 5G connectivity such as business enterprises and network equipment initially uses system integrators to create network infrastructure. This architecture will assist these organizations to augment operational efficiency in less time. Further, the growing demand for cloud-driven applications across verticals is also projected to supplement the requirement for application integration in the upcoming years.

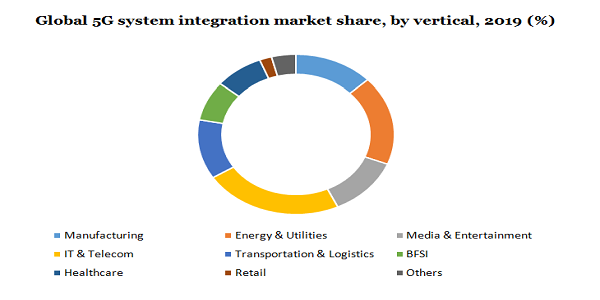

The IT & Telecom division occupied 25.1% of the 5G system integration market share in 2019, owing to the increasing demand for integration services in IT & telecom organizations to assist 5G infrastructure. With the growing emphasis on offering seamless connectivity on virtual meetings to lower the travel time of a specialist or consultant, the preference for 5G infrastructures is predicted to showcase wide acceptance across various verticals in the coming years. Thus, the increasing demand for 5G systems is projected to foresee considerable growth for implementing the infrastructure in the organizations.

Owing to the growth of digitalization in the manufacturing industry, automation has become the new norm as it enhances overall efficiency. This has driven the demand for uninterrupted wireless communication between industrial sensors, robots, and other devices. Thus, the manufacturing industry is predicted to ascend with a steady CAGR in the upcoming years due to increasing demand for system integration to combine the entire facility with 5G infrastructure.

The home & office broadband division held the largest market share of 23.8% in 2019 owing to increasing demand for system integration to offer improved mobile broadband to enterprises and customers. Further, a rapid increase in IoT-enabled devices across smart cities is predicted to supplement the demand for system integration to make devices compatible with the new 5G technology.

The penetration of collaborative robots and connected sensors is estimated to grow substantially worldwide in the upcoming years. The intelligent power distribution systems division is anticipated to foresee considerable growth, due to seamless communication set-up in smart grids to mechanize the storage and distribution operations.

North America occupied a 34.1% share in 2019 and is expected to grow with a significant growth rate over the estimated duration. The operation of large telecom and IT players are predicted to boost market growth in the upcoming years. Further, increasing investments in implementing the 5G eco-system by leading players are anticipated to accelerate product usage across various industries such as healthcare, IT & Telecom, and energy & utilities over the estimated period.

In the Asia Pacific region, leading telecom players such as SK Telecom, China Mobile, and KT Corporation are making considerable investments in 5G networks in South Korea, China, and Japan. Rapidly growing investments for implementing 5G infrastructure in various verticals are projected to generate new growth avenues in the coming years. Moreover, the growth of small and medium IT players in developing nations such as India and China is predicted to drive the product demand over the forecast period.

There has been a shift towards network usage from office premises to individual premises following the outbreak of COVID-19. In addition, internet traffic has witnessed significant growth as people are forced to stay in their homes. However, owing to the decline in enterprise internet consumption, the demand for high-speed internet may not be the same as it was at the beginning of 2020. This has led to a reduction in capital expenditure on the development of the 5G network. However, this reduction in Capex and limited workforce to roll out the 5G technology are estimated to affect the market for the short term. Once the world’s major economies recover, there would be significant investment in the development of 5G infrastructure.

The key players of the market include ALTRAN; Accenture Inc.; Tata Consultancy Services Limited; Keysight Technologies; Huawei Technologies Co., Ltd.; Infosys Limited; Oracle Corporation; Radisys Corporation; Samsung Electronics Co., Ltd.; IBM Corporation; ECI TELECOM; HCL Technologies Limited; AMDOCS; CA Technologies; HPE; Cisco Systems, Inc.; Sigma Systems; Wipro Limited; and Ericsson. The leading players emphasize making investments in developing systems, platforms, software, and other solutions to improve their product offering. For example, Huawei Technologies plans to invest USD 350 million in the next three years. This investment is predicted to develop integrated services such as platforms, consulting services, and tools driven by the 5G system.

The key players are undertaking alliances and entering agreements to acquire more market share. For example, HPE in February 2019 collaborated with Samsung Electronics Co., Ltd. This collaboration is aimed at providing edge-to-core virtual vRAN solutions built on Samsung’s system and radio network infrastructure. HPE invested around USD 4 billion to launch covered edge solutions that target to offer to Communication Service Providers (CSP) and other cases such as video analytics, IoT, and media streaming.

|

Report Attribute |

Details |

|

The market size value in 2020 |

USD 7.02 Billion |

|

The revenue forecast in 2027 |

USD 31.41 Billion |

|

Growth Rate |

CAGR of 23.8% from 2020 to 2027 |

|

The base year for estimation |

2019 |

|

Historical Data |

2019 |

|

Forecast period |

2020 - 2027 |

|

Quantitative units |

Revenue in USD million and CAGR from 2020 to 2027 |

|

Report coverage |

Revenue forecast, company ranking, competitive landscape, growth factors, and trends |

|

Segments covered |

Services, vertical, application, region |

|

Regional scope |

North America; Europe; Asia Pacific; Latin America; MEA |

|

Country scope |

U.S.; Canada; U.K.; Germany; France; Italy; Russia; China; Japan; India; South Korea; Mexico; Brazil |

|

Key companies profiled |

Accenture Inc.; Huawei Technologies Co., Ltd.; Cisco Systems, Inc.; Infosys Limited; Tata Consultancy Services Limited; Wipro Limited; Radisys Corporation; IBM Corporation; HPE; Oracle Corporation; HCL Technologies Limited; ALTRAN; AMDOCS; CA Technologies; Samsung Electronics Co., Ltd.; Ericsson; Keysight Technologies |

|

Customization scope |

Free report customization (equivalent to up to 8 analysts’ working days) with purchase. Addition or alteration to country, regional & segment scope. |

|

Pricing and purchase options |

Avail of customized purchase options to meet your exact research needs. |

This report forecasts revenue growth at global, regional, and country levels and provides an analysis of the latest industry trends in each of the sub-segments from 2019 to 2027. For the purpose of this study, Million Insights has segmented the global 5G system integration market report based on services, vertical, application, and region:

• Services Outlook (Revenue, USD Million, 2019 - 2027)

• Consulting

• Infrastructure Integration

• Application Integration

• Vertical Outlook (Revenue, USD Million, 2019 - 2027)

• Manufacturing

• Energy & Utility

• Media & Entertainment

• IT & Telecom

• Transportation & Logistics

• BFSI

• Healthcare

• Retail

• Others

• Application Outlook (Revenue, USD Million, 2019 - 2027)

• Smart City

• Collaborate Robot/ Cloud Robot

• Industrial Sensors

• Logistics & Inventory Monitoring

• Wireless Industry Camera

• Drone

• Home and Office Broadband

• Vehicle-to-Everything (V2X)

• Gaming and Social Media

• Remote Patient & Diagnosis Systems

• Intelligent Power Distribution System

• P2P Transfers/ mCommerce

• Others

• Regional Outlook (Revenue, USD Million, 2019 - 2027)

• North America

• U.S.

• Canada

• Europe

• U.K.

• Germany

• France

• Russia

• Italy

• the Asia Pacific

• China

• India

• Japan

• South Korea

• Latin America

• Brazil

• Mexico

• Middle East & Africa (MEA)

Research Support Specialist, USA