- US: +1-408-610-2300

- Toll Free: +1-866-831-4085

- Become a Client

The global aerospace and defense maintenance, repair, and overhaul (MRO) market size was accounted for USD 111.68 billion in 2018. It is expected to witness growth with a 5.4% CAGR over the forecasted years, 2019 to 2025. This growth can be associated with surging air travel demand across the globe coupled with fleet renewal delay on account of reduced fuel prices.

Developing economies like the Middle East and the Asia Pacific are anticipated to witness more growth in the upcoming years. This growth is possible on account of the increase in spending by several airlines for MRO (Maintenance, Repair & Overhaul) of aircraft due to surging air traffic. On the other hand, the market across North America and Europe is expected to register a steady growth rate owing to a modest rate of expansion of fleets.

The U.S. dominated the global market with a share of 22.9% in 2018. But, it is anticipated to register low growth in the upcoming years on account of shifting companies across the Asia Pacific region owing to skilled labor availability and low labor costs. However, surging investments being made in the defense sector for the purchase of advanced aircraft are expected to drive market growth in the upcoming years.

Several OEMs have started the adoption of enhanced business models which allowed suppliers to act as system integrators. Developing economies have started witnessing an increase in MRO players on account of collaborations and ventures among aircraft manufacturers and system suppliers coupled with lower labor costs.

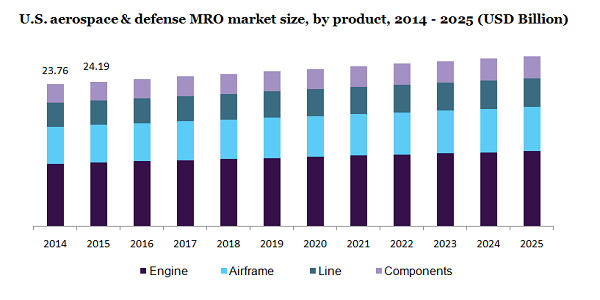

In 2018, the engine product segment held the largest share of 38.1% across the overall global market. This can be associated with the surging fleet expansion and an increased number of mature engines like V2500 and CFM56. This product segment is anticipated to witness competition on account of the incorporation of OEMs.

The line maintenance product segment is expected to register the highest CAGR in the upcoming years. It is anticipated to generate revenue of USD 31.15 Billion by 2025. This can be associated with the need for mandatory maintenance of aircraft at regular intervals of time. Several airlines are outsourcing line maintenance of aircraft and similar other services on account of its cost-effective nature.

The application segment of Narrow Body Aircraft held the largest share across the global market in 2018. This segment is expected to generate a revenue of USD 86.50 Billion by 2025. This can be associated with the usage of these aircraft owing to their features like low-operational costs, higher fuel efficiency, and more takeoff weight.

The Wide Body Aircraft segment is also expected to grow at significant growth in the upcoming years. This growth can be attributed to its feature of enhanced average life. Also, other features like increased international air traffic are projected to drive growth. Moreover, the launching of fuel-efficient aircraft like Airbus is anticipated to drive the demand for this segment across the globe.

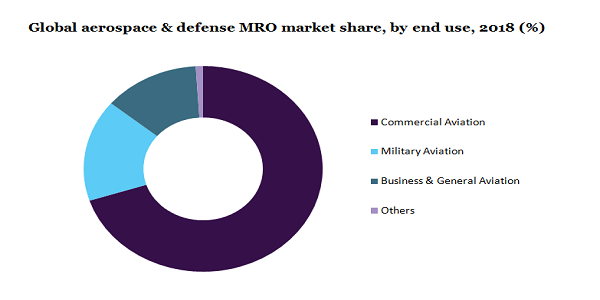

In 2018, the commercial aviation segment dominated the global aerospace & defense MRO market. It is also anticipated to register a 5.8% CAGR during the forecasted years, 2019 to 2025. This growth can be attributed to the rising number of airline fleets to accommodate surging cargo and passenger traffic. Also, increased maintenance costs coupled with technological advances being made in this sector are expected to propel market growth.

Increased military spending for the purchase of advanced aircraft like attack and assault helicopters which provide to be boon in aerial warfare is expected to create opportunities for military purposes. Also, the rising usage of airplanes and helicopters for transporting weapons, military equipment, and troops is expected to pave the way for the demand for such systems.

In 2018, North America dominated the global aerospace & defense maintenance, repair & overhaul market. This can be attributed to an increase in military spending coupled with surging passenger traffic. But, this market is expected to witness modest growth on account of the matured aerospace industry across countries like the U.S. Further, problems related to skilled laborers are also expected to contribute to moderate market growth across this region.

The Asia Pacific is expected to register the highest growth with 8.8% during the forecasted years, 2019 to 2025. This can be associated with the shifting trend of MRO activities from Europe and North America on account of low labor costs, skilled workforce, and advantage in the supply chain.

The outbreak of the COVID-19 virus has negatively impacted the global aerospace & defense MRO (maintenance, repair, and overhaul) market. The imposition of lockdown and travel restrictions has stagnated the growth of the aviation industry. Thus, many passenger and commercial planes have restricted their number of travel journeys or either have canceled their flights. Also, hindrances in the operations like tourism, supply chain, entertainment, and coupled with the fluctuations in the air-fuel prices have severely affected the players operating in the aviation industry. This has resulted in financial loss and bankruptcy. But, an expected surge in the number of air travelers willing to return to their hometown is anticipated to trigger the demand for aerospace & defense MRO over the post-pandemic period.

This market is anticipated to witness competition due to OEM integration in the value chain. They have started offering purchase packages of longer duration for increasing their presence in the aftermarket. Several airlines are outsourcing services for reducing repair and maintenance costs.

The key players in this market are AAR Corporation, GE Aviation, Boeing Company, Honeywell Aerospace, Bombardier Inc., Airbus SAS, Delta TechOps, and Safran SA. They are engaged in product development and innovation to gain a competitive advantage over other players. Also, marketing strategies like mergers and acquisitions are being carried out by these players for their reach.

|

Attribute |

Details |

|

The base year for estimation |

2018 |

|

Actual estimates/Historical data |

2014 - 2017 |

|

Forecast period |

2019 - 2025 |

|

Market representation |

Revenue in USD Million and CAGR from 2019 to 2025 |

|

Regional scope |

North America, Europe, Asia Pacific, Central & South America, Middle East & Africa |

|

Country Scope |

U.S., Canada, Mexico, Germany, U.K., France, Italy, Spain, China, India, Japan, Australia, Indonesia, Malaysia, Singapore, Brazil, Argentina, UAE, Saudi Arabia |

|

Report coverage |

Revenue forecast, company share, competitive landscape, and growth factors and trends |

|

15% free customization scope (equivalent to 5 analyst working days) |

If you need specific information, which is not currently within the scope of the report, we will provide it to you as a part of the customization |

This report forecasts revenue growth at the global, regional, and country levels and provides an analysis of the latest industry trends from 2014 to 2025 in each of the sub-segments. For the purpose of this study, Million Insights has segmented the global aerospace and defense MRO market report based on product, application, end-use, and region:

• Product Outlook (Revenue, USD Million, 2014 - 2025)

• Engine

• Airframe

• Line

• Component

• Application Outlook (Revenue, USD Million, 2014 - 2025)

• Narrow Body Aircraft

• Wide Body Aircraft

• Regional Aircraft

• Others

• End-Use Outlook (Revenue, USD Million, 2014 - 2025)

• Commercial Aviation

• Business & General Aviation

• Military Aviation

• Other

• Region Outlook (Revenue, USD Million; 2014 - 2025)

• North America

• U.S.

• Canada

• Mexico

• Europe

• Germany

• U.K.

• France

• Italy

• Spain

• the Asia Pacific

• China

• India

• Japan

• Australia

• Indonesia

• Malaysia

• Singapore

• Central & South America

• Brazil

• Argentina

• Middle East

• UAE

• Saudi Arabia

• Africa

Research Support Specialist, USA