- US: +1-408-610-2300

- Toll Free: +1-866-831-4085

- Become a Client

The global radar market size was accounted for the revenue of USD 29.46 billion in 2018. It is expected to witness growth with a CAGR of 3.8% over the forecasted years, 2019 to 2025. This growth can be attributed to the rising usage of these radars for military and defense purposes across national borders. Moreover, surging travel activities and sea trade are further anticipated to drive market growth in the upcoming years.

Rising concerns about security and safety coupled with increased defense budgets are expected to propel the demand for radar systems. In addition, the rising construction of new terminals and airports is anticipated to drive the demand for such radars. Moreover, an increasing number of conflicts between countries, terrorism, and infiltrations across the borders is projected to create opportunities for the global market.

The usage of sensors that are radar-based is gaining popularity in airplanes, railways, and automobiles. This can be associated with their features like resistance against harsh weather conditions, high range detection, and flexible mounting. Moreover, rising sea trade along the international borders coupled with the need for goods movement has boosted the need for increasing sizes of merchant vessels and fleets. Thus, radar systems are being used for tracking such vessels.

Various governing authorities have imposed stringent rules for continuous surveillance at airports due to a large number of travelers and goods transportation. Thus, the airport operators are insisting on enhancing the system of runway safety coupled with the deployment of systems having radio detection technology.

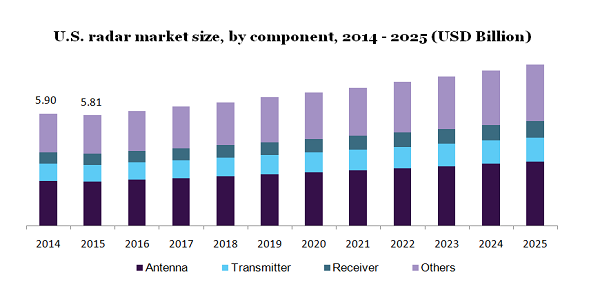

The segment of the antenna is anticipated to hold the largest share across the global market from 2019 to 2025. This can be associated with surging demand for the processing of digital signals. Moreover, the rising deployment of radar systems coupled with the need for upgrading the existing ones is further projected to drive the market growth during the forecasted years.

In 2018, the transmitter segment held a share of around 16% across the global market. This can be attributed to their usage for the creation of frequency pulses having high power and short duration. These pulses are further radiated by connected antennas. Out of many available transmitters, the PAT (Power Amplifier Transmitters) and POT (Power Oscillator Transmitters) are prominently used across the globe for the manufacturing of radar systems.

The service segment of installation/integration is projected to hold the largest share across the global market by the end of 2025. This growth can be attributed to the rising demand for the mounting radars on airplanes and specialized vehicles coupled with the increased air traffic across the globe.

The need for timely and regular maintenance of radars is expected to boost the growth for the segment of support & maintenance. It is also expected to hold significant growth by 2025. Moreover, the rising rate of deployment and dominance of radars is projected to proliferate the growth of the segment.

In 2018, the segment of airborne platforms generated a revenue of USD 8,866.9 Million across the global market. This can be associated with surging needs across the majority of the aircraft for good performance in missions. These military missions have varied requirements in terms of range, distance, strike rate, target types, and environmental effects which require varied sets of waveforms. Moreover, the rising number of commercial aircraft fleets is further expected to drive market growth in the upcoming years.

In addition, the influence of ground base systems is increasing on account of the rising need for locating the targets and strengthening of the cavalry units. The key player in the market named Lockheed Martin Corporation has developed antennas with DART technology. Such factors are further anticipated to fuel up the market growth in the upcoming years.

In 2018, the segment of X-band held the second-largest share across the global market. This can be attributed to its usage across large vessels and ships for sea surface area monitoring. Moreover, factors like the rising number of offshore installations and surging usage for navigation and traffic control are anticipated to promote the segment growth. This segment is anticipated to hold the largest share across the market by the end of 2025.

The S-band radar segment is also gaining popularity across the globe owing to its rising deployments across large antennas for performing maritime operations. They are mainly used for applications like bird detection through long-range and good visibility even in extreme weather conditions & precipitation during flights. Moreover, the rising demand for communication satellites is further expected to drive the segment growth.

The long-range end use segment held the largest share across the global market. This growth can be attributed to its surging usage in the defense and aerospace sectors. They are being used for meeting the objective of surveillance like target location and weapon detection. Moreover, rising expenditure on defense across countries like Russia, India, and Brazil is further anticipated to drive market growth in the upcoming years.

These long-range radars can also be used for the detection of multiple targets along with ongoing surveillance functions. They are also being used for target detection from high to ultra-low altitudes. Moreover, their mobile configurations can help them to withstand all types of environments.

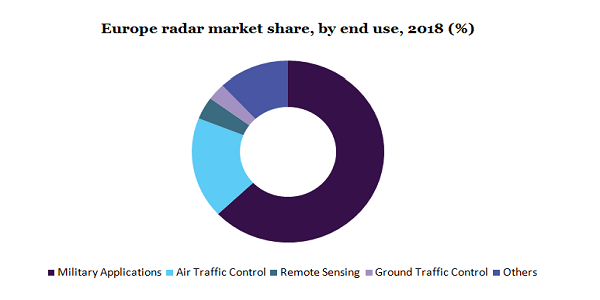

In 2018, the military end-use segment held the largest share across the global market. This can be associated with an increasing need for such detection systems being used for fire control, surveillance, vehicle search, and ATC (Air Traffic Control). In the previous days, these radars were being used only for military applications but rapid advancements in technology have made them useful across medical, industrial, and commercial applications.

The air traffic control segment held the second-largest share across the global market and is anticipated to continue its growth in the upcoming years. This growth can be attributed to an exponential rise in cargo planes and flight frequency. Moreover, rising demand for air traffic has surged the need for traffic control for the prevention of fatal encounters. These factors are anticipated to boost the segment's growth.

The Asia Pacific held the second-largest share across the global radar market in 2018. This can be attributed to several factors like increasing manufacturing bases, SME’s presence, surging adoption of radar technology, and boosting sea trade between the countries. Moreover, rising investments being made across countries like China for promoting R&D activities are further anticipated to drive market growth in the upcoming years.

North America is also anticipated to witness substantial growth in the upcoming years. In addition, research activities like the development of quantum radar for stealth aircraft detection are being carried out in Canada. Such technology can be used to detect objects in a more precise and accurate form than the traditional systems. The research on these activities is under trial mode at the University of Waterloo and is anticipated to get launched in 2025.

The global radar market has boosted on account of the ongoing COVID-19 pandemic. The surging need to monitor movements of quarantine personnel coupled with the adoption of higher surveillance zones is expected to trigger the demand for radars across the globe. Also, the adoption of geotagging mobile applications in smartphones is being promoted by governing bodies to maintain social distancing. But, since the Asia Pacific is the home for several manufacturers and raw material suppliers, hindrance in their supply chain is expected to hamper the market growth to some extent. Moreover, economic and political tensions are expected to hinder the market demand over the post-pandemic period.

The market for radar includes key players like Collins Aerospace; Lockheed Martin Corporation; BAE Systems; Saab AB; Thales Group and Raytheon Company. In addition, other players like Northrop Grumman Corporation are continuously innovating and developing reliable radar systems that can be used for military surveillance.

These players are engaged in producing the radars that can be used systems being used for ground and air traffic monitoring. Moreover, the surging need for air traffic management coupled with the precise location information about the flights is further anticipated to drive the market in the upcoming years.

|

Attribute |

Details |

|

The base year for estimation |

2018 |

|

Actual estimates/Historical data |

2014 - 2017 |

|

Forecast period |

2019 - 2025 |

|

Market representation |

Revenue in USD Million and CAGR from 2019 to 2025 |

|

Regional scope |

North America, Europe, Asia Pacific, Latin America, and Middle East & Africa |

|

Country Scope |

U.S., Canada, Germany, U.K., China, India, Japan, and Brazil |

|

Report coverage |

Revenue forecast, company share, competitive landscape, and growth factors and trends |

|

15% free customization scope (equivalent to 5 analyst working days) |

If you need specific information, which is not currently within the scope of the report, we will provide it to you as a part of the customization |

This report forecasts revenue growth at the global, regional, and country levels and provides an analysis of the latest industry trends from 2014 to 2025 in each of the sub-segments. For the purpose of this study, Million Insights has segmented the global radar market report based on component, service, platform, frequency band, range, end-use, and region:

• Component Outlook (Revenue, USD Million, 2014 - 2025)

• Antenna

• Transmitter

• Receiver

• Others

• Service Outlook (Revenue, USD Million, 2014 - 2025)

• Installation/Integration

• Support & Maintenance

• Training & Consulting

• Platform Outlook (Revenue, USD Million, 2014 - 2025)

• Ground-based

• Naval

• Airborne

• Space-based

• Frequency Band Outlook (Revenue, USD Million, 2014 - 2025)

• L-band

• S-band

• C-band

• X-band

• Ku-band

• Ka-band

• Others

• Range Outlook (Revenue, USD Million, 2014 - 2025)

• Long

• Medium

• Short

• End-Use Outlook (Revenue, USD Million, 2014 - 2025)

• Military Applications

• Air Traffic Control

• Remote Sensing

• Ground Traffic Control

• Others

• Regional Outlook (Revenue, USD Million, 2014 - 2025)

• North America

• U.S.

• Canada

• Europe

• Germany

• U.K.

• the Asia Pacific

• China

• India

• Japan

• Latin America

• Brazil

• Middle East & Africa

Research Support Specialist, USA