- US: +1-408-610-2300

- Toll Free: +1-866-831-4085

- Become a Client

The global thermoform packaging market size was worth USD 39.86 billion in 2018. The market is estimated to register a 4.7% CAGR from 2019 to 2025. Increasing packaged food demand and the booming retail sector are driving the growth of the market. Packaged foods such as seafood and meat products consumption have increased considerably in the recent past.

In thermoforming, plastic material is heated to the desired temperature before converting it into the required shape by molding. The process of thermoforming is classified into thick gauge and thin gauge thermoforming. Thin gauge thermoform includes trays & lids, clamshell, blisters, and others are increasingly used in the packaging of pharmaceuticals, home care products, and electronics.

Thermoform offers various advantages like quick development of product and prototyping, cost-effective production for smaller quantities, and lower tooling cost. These benefits make it more popular than other packaging methods such as rotational and injection molding. However, the rising focus on sustainable packaging is estimated to restrain the growth of plastic-based packaging including thermoform packaging.

The growing adoption of technologies like modified atmosphere technologies, which help in extending the packaged food’s shelf life is anticipated to bode well for the market growth. The increasing number of foodservice outlets use thermoform packaging products including trays, cups, and containers for parcel packaging and table offering.

The increasing trend of on-the-go consumption, ready-to-eat food, and single-serve is estimated to bolster the market growth over the forecast years. Increasing demand for trays, containers, and clamshells by foodservice operators is projected to spur market growth. However, stringent regulatory frameworks concerning plastic use are likely to obstruct the market growth from 2019 to 2025.

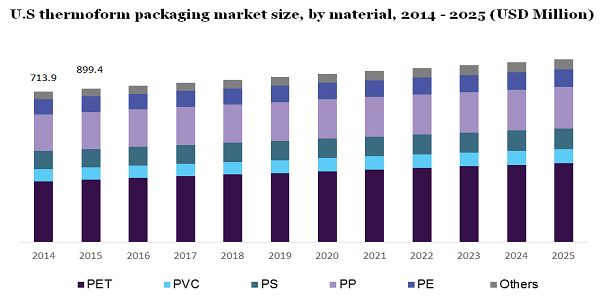

Based on the material, PET held the largest share in the thermoform packaging market in 2018. Factors such as the growing focus on using recyclable materials and reducing plastic packaging are supplementing the growth of this segment.

On the other hand, the PE segment is anticipated to register the maximum growth over the forecast duration. The rise in the demand for skin packaging is attributing to the growth of this packaging. PE consists of HDPE and LDPE of which the former is used to manufacture trays for food service and industrial packaging while the latter is used for packaging of seafood and meat products. Factors such as increasing the frozen meat industry and rising penetration of retail sectors are driving the growth of this segment.

Polypropylene (PP) is one of the most used materials in the packaging industry. It is a robust and tough plastic material and displays favorable characteristics such as clarity, strength, high resistance to puncture and heat. Owing to these properties, it is widely used in various applications. PP helps in retaining the freshness of food products, thereby; it is increasingly preferred in the packaging of food products.

Depending on the product, the container segment held the highest share in the market by revenue with over 26.0% in 2018. Increasing the use of thermoforming containers in the foodservice industry is the major factor driving the product demand. Moreover, the rise in food delivery services in emerging countries is further attributing to the growth of this segment. Containers are hollow products used to hold products. Containers are used for various food products such as fresh fruits, prepared meals, frozen food, bakery food, and dried foods.

The clamshell segment is estimated to register the highest growth over the forecast duration, and it is projected to account for USD 8,582.2 million by 2025. It is increasingly used in several end-use industries like homecare, electronics, and others. Clamshell has multiple advantages such as lucrative design, easy to use, tamper-evident features, and transparency. These benefits drive its application across different end-use industries.

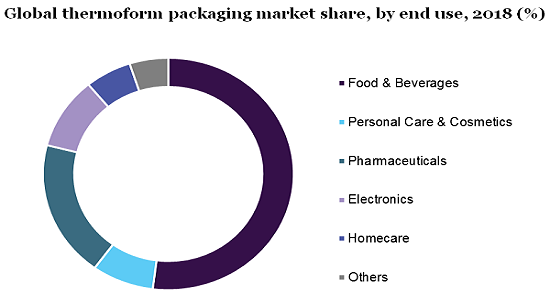

Depending on the end-use, the food and beverage segment occupied the largest share in the market with 51.6% by revenue in 2018. In addition, the segment is estimated to register considerable growth owing to the rising demand for thermoform containers for dairy products packaging. Further, advancements in thermoform technology and increasing demand for lightweight packaging are projected to bolster the segment growth.

On the other hand, the pharmaceuticals segment is projected to register considerable growth over the forecast duration. The demand for blister packaging is gaining traction among nutraceutical and pharmaceutical companies owing to easy unit dose packaging and its tamper-evident features.

Electronics is another major application that uses blister packaging for the packaging of mobile accessories, headphones, and batteries among others. E-commerce plays a vital role in the sales of electronics products. The rapid rise in the e-commerce sector, especially, in emerging countries is projected to bolster the segment growth. Apart from blister packaging, clamshells packaging is estimated to register considerable growth in the packaging of electronics items.

In 2018, North America occupied the highest share in the market. Further, the region is anticipated to continue its dominance from 2019 to 2025. The region has a sizeable presence of large-sized foodservice and packaged food industries, which are contributing to the growth. In addition, North America has also a considerable presence of thermoform packaging manufacturers. The introduction of new products by these companies is anticipated to bode well for the growth of the market.

Asia Pacific is projected to emerge as the highest growing region with a 6.8% CAGR over the forecast duration. Factors such as rising penetration of online food delivery services and ready meals demand are attributing to the growth of the regional market. In addition, the expansion of the pharmaceuticals industry in the Asia Pacific is projected to drive the demand for thermoform packaging industries.

Thermoform packaging industry has been adversely affected due to the outbreak of the COVID-19 pandemic. Packaging companies along with end-use industries were forced to shut their operations owing to the international lockdown. The food and beverage end-use segment, which occupies over half the market share in thermoform packaging, has been hit badly owing to the closure of retail stores and foodservice outlets.

However, the pandemic has witnessed increased demand for online food services and pharmaceuticals products. Post lockdowns, these sectors are projected to register considerable growth and help the thermoform packaging industry in its recovery.

The market is highly competitive owing to the presence of both international and domestic players. Product differentiation is the major strategic initiative adopted by market players to gain a competitive edge over others. In 2018, Pactiv LLC has emerged as the leader in the market owing to its wide presence in North America, and an increasing number of products for the food & beverage industries.

Key players operating in the market are Placon Corporation, WestRock Company, Huhtamaki Group, Anchor Packaging, Inc., Tray-Pak Corporation, DS Smith Plc, and Pactiv LLC among others. These companies are focusing on the introduction of new products to strengthen their presence in the global market.

|

Attribute |

Details |

|

The base year for estimation |

2018 |

|

Actual estimates/Historical data |

2014 - 2017 |

|

Forecast period |

2019 - 2025 |

|

Market representation |

Revenue in USD Million and CAGR from 2019 to 2025 |

|

Regional scope |

North America, Europe, Asia Pacific, Central & South America, Middle East & Africa |

|

Country Scope |

U.S., Canada, Mexico, Germany, Italy, France, UK, China, India, Japan, Brazil, Saudi Arabia |

|

Report coverage |

Revenue forecast, competitive landscape, growth factors, and trends |

|

15% free customization scope (equivalent to 5 analysts working days) |

If you need specific market information, which is not currently within the scope of the report, we will provide it to you as a part of the customization |

This report forecasts revenue growth at global, regional, and country levels, and provides an analysis of the latest industry trends in each of the sub-segments from 2014 to 2025. For this study, Million Insights has segmented the global thermoform packaging market based on material, product, end-use, and region:

• Material Outlook (Revenue, USD Million; 2014 - 2025)

• PET

• PVC

• PS

• PP

• PE

• Others

• Product Outlook (Revenue, USD Million; 2014 - 2025)

• Blister Packaging

• Clamshell Packaging

• Skin Packaging

• Trays & Lids

• Containers

• Others

• End-Use Outlook (Revenue, USD Million; 2014 - 2025)

• Food & Beverage

• Personal Care & Cosmetics

• Pharmaceuticals

• Electronics

• Homecare

• Others

• Regional Outlook (Revenue, USD Million; 2014 - 2025)

• North America

• The U.S.

• Canada

• Mexico

• Europe

• Germany

• Italy

• France

• UK

• The Asia Pacific

• China

• India

• Japan

• Central & South America

• Brazil

• Middle East & Africa

• Saudi Arabia

Research Support Specialist, USA