- US: +1-408-610-2300

- Toll Free: +1-866-831-4085

- Become a Client

The global smart electricity meters market size was worth USD 10.0 billion in 2019. It is anticipated to exhibit a 7.8% CAGR over the forecast period, 2020 to 2027. Smart meters are used to record various information such as electricity consumption, power factor, current, and voltage levels. These meters provide information to the consumers regarding their consumption behavior, thereby, helping them to reduce unnecessary electricity consumption. Energy suppliers use this technology to reduce the reaction time in resolving hardware faults.

Despite the advancements in metering systems, energy theft may occur either before the measurement of demand or after the transmission of measurement logs to the utility. Different tampering method includes saturation of inbuilt magnetic components as well as brute force technique like jamming mechanism deployment.

Intelligent metering systems are integrated into a data simulator that predicts the energy requirement for the future based on the current energy needs, thus, offering advantages to both energy providers and consumers. In addition, smart electricity meters help in controlling the emission of radiation. Stringent regulations about radiation emission are likely to spur the deployment of smart meters. For example, in the U.K, the Department of energy and Climate Change monitor the timely installation of smart electric meters. Owing to the growing need to abide by the regulations, manufacturers are estimated to introduce new products, thereby, increasing the competition in the market. Further, increasing the promotion of green energy coupled with the efficient transmission is likely to supplement the product demand.

Intelligent metering systems are integrated into a data simulator that predicts the energy requirement for the future based on the current energy needs, thus, offering advantages to both energy providers and consumers. In addition, smart electricity meters help in controlling the emission of radiation. Stringent regulations about radiation emission are likely to spur the deployment of smart meters. For example, in the U.K, the Department of energy and Climate Change monitor the timely installation of smart electric meters. Owing to the growing need to abide by the regulations, manufacturers are estimated to introduce new products, thereby, increasing the competition in the market. Further, increasing the promotion of green energy coupled with the efficient transmission is likely to supplement the product demand.

Smart meters provide energy forecast and analysis that is not possible by conventional systems. With the sophistication in technology, the intelligent metering system is estimated to prevent energy theft. Sharing information in real-time regarding tariff rates ad usage offers a competitive advantage. In addition, the rise in awareness about the advantages of these devices is likely to drive their adoption.

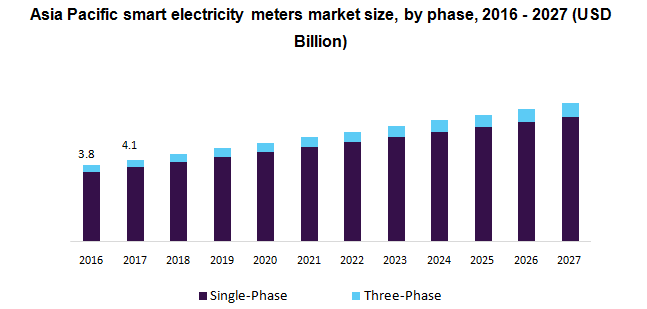

Depending on the phase, the smart electricity meters market is classified into three-phase and single phases. It is predicted that the three-phase category would exhibit the highest growth rate compared to the single-phase. The rise in the installation of smart meters in commercial and industrial applications is attributing to the growth of this segment. Three-phase meters can handle more loads along with offering flexibility by dividing the load into three phases.

The rise in industrial and commercial infrastructure development in emerging countries is anticipated to boost the three-phase growth further. In addition, owing to the flexibility of these meters, there is gaining traction in residential applications as well. On the other hand, single-phase systems are mostly used for industrial applications where there is a lesser consumption of electricity.

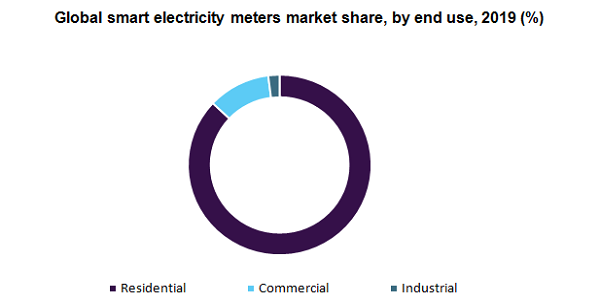

Based on the end-user, the market is segmented into commercial, industrial and residential. Further, the residential category includes standalone bungalows and suburban/urban apartments. The commercial segment comprises all commercial infrastructure such as offices, hotels, and shopping malls among others while the industrial end-use segment mainly includes processing plants and manufacturing units.

In 2019, the residential segment dominated the smart electricity meter market due to the growing focus on the promotion of energy conservation and increasing awareness regarding the benefits of smart meters. As per the U.S Energy Information Administration, out of 86.8 million smart meters in the U.S, nearly 88% are installed for residential applications. On the other hand, the commercial segment is also estimated to witness significant growth owing to the rapid infrastructural development in developing economies.

Globally, Asia Pacific has the highest number of smart meters owing to the stringent regulations that mandate the installation for various commercial, residential and industrial applications. Further, the region is estimated to register over 9% CAGR by revenue over the forecast duration. China is aiming for sustainable energy management, which is further anticipated to contribute to regional growth. The residential sector is likely to be the most lucrative in the region. Further, smart city projects in India are likely to drive intelligent electricity meters adoption.

North America also held a significant share in the market owing to the increasing number of houses with smart meters. In addition, increasing focus by governments and consumers awareness attribute to the growth of the residential sector in the region. On the other hand, Europe is witnessing the rapid installation of smart electricity meters. As of 2020, members of the European Union have reported to roll out nearly 200 million smart meters. By the end of 2020, it is projected that nearly 72% of consumers will have smart meters.

COVID-19 has delayed the installation of smart electricity meters in different parts of the world. This delay has been caused due to the lack of a workforce to carry out the installation and supply chain disruption caused by the pandemic. In addition, governments across the globe have halted various infrastructural development projects amid the economic onslaught. This has further affected the market growth.

However, with the resumption of economic activities, various infrastructural projects have restarted. Members of the European Union are anticipated to provide smart meter installation to over 70% of its consumers by the end of 2020. Such initiatives provide a lucrative opportunity for the growth of the market.

Key players involved in the market are Iskraemecod.d, Landis+Gyr, Itron Inc., Elster Group GmbH, ABB, Siemens, Schneider Electric, and GENERAL ELECTRIC among others. By undertaking various strategic initiatives, market players are focusing on increasing their customer base. Various strategic initiatives include partnerships, mergers & acquisitions, and geographical expansion. For example, Aclara Technologies LLC, in 2017, acquired most of the equity interest in General Electric Philippines Meter and Instrument Co. By this acquisition, the company started a joint venture named GEPMICI with an aim to expand its reach in the Philippines market.

|

Attribute |

Details |

|

The base year for estimation |

2019 |

|

Actual estimates/ Historical data |

2016 - 2018 |

|

Forecast period |

2020 - 2027 |

|

Market representation |

Volume in Thousand Units, Revenue in USD Million, and CAGR from 2020 to 2027 |

|

Region scope |

North America, Europe, Asia Pacific, South America, MEA |

|

Country scope |

U.S., Canada, Mexico, Germany, U.K., France, Spain, Italy, Netherlands, China, Japan, South Korea, and Brazil |

|

Report coverage |

Revenue forecast, company share, competitive landscape, growth factors, and trends |

|

15% free customization scope (equivalent to 5 analysts working days) |

If you need specific information that is not currently within the scope of the report, we will provide it to you as a part of the customization |

This report forecasts revenue growth at global, regional, and country levels, an analysis of the latest industry trends in each of the sub-segments from 2016 to 2027. For the purpose of this study, Million Insights has segmented the global smart electricity meters market report based on phase, end-use, and region:

• Phase Outlook (Revenue, USD Million, 2016 - 2027)

• Single-phase

• Three-phase

• End-use Outlook (Volume, Thousand Units; Revenue, USD Million, 2016 - 2027)

• Residential

• Commercial

• Industrial

• Regional Outlook (Volume, Thousand Units; Revenue, USD Million, 2016 - 2027)

• North America

• U.S.

• Canada

• Mexico

• Europe

• Germany

• U.K.

• France

• Italy

• Spain

• Netherlands

• The Asia Pacific

• China

• Japan

• South Korea

• South America

• Brazil

• Middle East and Africa (MEA)

Research Support Specialist, USA