- US: +1-408-610-2300

- Toll Free: +1-866-831-4085

- Become a Client

The U.S. automotive collision repair market size was worth USD 33.75 billion in 2018, growing at 1.5% CAGR from 2019 to 2025. In the United States, it has mandated by the government and auto manufacturers to have active car insurance. The main objective behind insurance is to enable car owners to bear the expenses of damaged caused to the vehicles by accidents. Thus, mandatory insurance cover is likely to propel market growth over the next six years.

Increasing telematics adoption in the U.S. automotive industry is further anticipated to spur market growth. Technically advanced telematics helps in recording real-time vehicle data and sync the retrieved data with servers. Telematics devises logs are decoded through specific systems available at certified repair shops. Thus, this solution gives an edge to the repair shops owned by companies.

Technical advancements in collision repair and mandatory modification in insurance policies have positively affected the market growth. Standard and shared guidelines for automotive damaged repair parts have ensured transparency and efficiency. Further, technologies have helped in streamlining the repair and appraisal processes. Moreover, customers get information about the repairing works in real-time.

Technical advancements in collision repair and mandatory modification in insurance policies have positively affected the market growth. Standard and shared guidelines for automotive damaged repair parts have ensured transparency and efficiency. Further, technologies have helped in streamlining the repair and appraisal processes. Moreover, customers get information about the repairing works in real-time.

The United States accounts for a significant number of automotive sales. Factors such as high disposable income and increasing living standards have influenced vehicle demand. Therefore, the increasing number of automotive sales positively affectsU.S. automotive collision repair market growth. In addition, the country has stringent regulations pertaining to carbon emission, which has led to the increasing use of aluminum.

Key players operating in the industry are focusing on partnerships and collaboration to increase their market share. This allows them to cater to the increasing demand for aluminum-based components. Key players such as Nissan Motors, Kia Motors, Hyundai Motors, and Infiniti Global have witnessed nearly 20% growth in the sales of automotive vehicles and together they have opened 3,600 shops. This factor is projected to increase the demand for the automotive collision repair market.

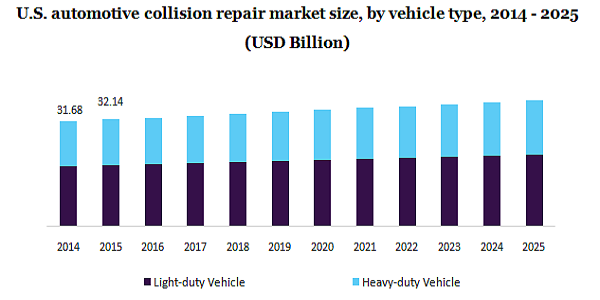

Depending on the vehicle type, the market is categorized into heavy-duty vehicles and light-duty vehicles. Light-duty vehicles accounted for the highest share in the market in 2018. Further, the segment is likely to register the highest growth over the forecast duration. Growing demand for costly items such as performance tires, glass products, and electronic mirrors is driving the growth of this segment.

In the United States, light-duty vehicles have gained traction in the past few years owing to stringent regulations pertaining to the use of heavy components in vehicle manufacturing. On the other hand, collision repair of heavy-duty vehicles depends on troubleshooting, comprehensive repairs, and truck repair maintenance. On the rolled trucks, animal hits, sandblasting & painting light collision, and other repair works are performed.

Based on product type, the U.S. automotive collision repair market is categorized into consumables, spare parts, paints & coatings. Of them, the spare parts segment accounted for the highest share in the market in 2018. On the other hand, the paint and coating division is estimated to register high growth from 2019 to 2025. Over the past few years, there has been advancement in the paints and coating used for automotive. Different types of painting include vehicle top coating, glass coatings, and electrodeposition coatings.

The spare parts category includes supplementary mechanical parts¸ automotive tools, repair materials, and crash parts. The rise in the sales of hybrid and electric vehicles has led to an increase in demand for spare parts, as these vehicles require specialized spare parts. Owing to this, there has been a rise in the number of car shops in the country specifically meant to repair hybrid and electric cars.

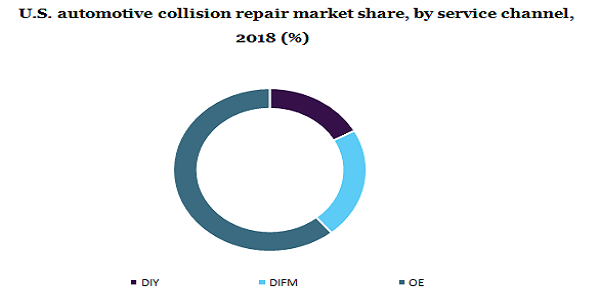

By service channel, the market is classified into OE, DIY, and DIFM. Of them, the OE category was the largest shareholder in the market in 2018. Several OEMs have developed their own channels to distribute branded parts to various DIFM. In addition, increasing car warranty services is further supplementing the growth of the market.

On the other hand, the DIY category is likely to account for a considerable share in the market over the forecast duration owing to the changing consumer preferences and increasing awareness about the replacement of various parts such as tires and headlights. DIFM segment is projected to register the highest growth over the forecast duration owing to the rising need for replacement of bigger parts such as suspension systems, clutch, and transmission components among others.

On the other hand, the DIY category is likely to account for a considerable share in the market over the forecast duration owing to the changing consumer preferences and increasing awareness about the replacement of various parts such as tires and headlights. DIFM segment is projected to register the highest growth over the forecast duration owing to the rising need for replacement of bigger parts such as suspension systems, clutch, and transmission components among others.

The market has been the worst hit due to the COVID-19 outbreak. The country has enforced restrictions on the operation of various businesses to contain the spread of coronavirus. With people staying indoors and work from home becoming new normal, there has been a significant decline in the number of on-road traffic. Thus, the country has witnessed a significantly fewer number of collision accidents, which, in turn, has led to a decline in the demand for this market. However, with the systematic opening of various businesses, automotive sales are anticipated to surge in the near future, thereby, helps in recovering the market.

Key companies in the market have been focusing on garnering a larger consumer base by providing online repair services. For example, Garage Gurus, Federal-Mogul Motorparts, through its technical education platform offer online, on-site and on-demand training and support services to various shop owners and technicians. In addition, Continental Collision is a certified collision repair center for major automotive manufacturers such as Nissan, Subaru, Infiniti, Honda, and Mercedes-Benz.

Key players are also focusing on mergers and acquisitions to consolidate their market presence. For example, Mann+Hummel Group, in 2016, acquired Affinia Group to enhance its product offering in the automotive collision repair market. Key players operating in the market are Valeo, 3M, ZF Friedrichshafen AG, Faurecia and Valeo among others.

|

Report Attribute |

Details |

|

The market size value in 2020 |

USD 35.0 billion |

|

The revenue forecast in 2025 |

USD 37.6 billion |

|

Growth Rate |

CAGR of 1.5% from 2019 to 2025 |

|

The base year for estimation |

2018 |

|

Historical data |

2014 - 2017 |

|

Forecast period |

2019 - 2025 |

|

Quantitative units |

Revenue in USD billion and CAGR from 2019 to 2025 |

|

Report coverage |

Revenue forecast, company ranking, competitive landscape, growth factors, and trends |

|

Segments covered |

Product type, vehicle type, the service channel |

|

Country scope |

The U.S. |

|

Key companies profiled |

ZF Friedrichshafen AG; Valeo; Federal-Mogul Corporation; Faurecia; Continental Corporation; 3M |

|

Customization scope |

Free report customization (equivalent to up to 8 analysts working days) with purchase. Addition or alteration to country, regional & segment scope. |

|

Pricing and purchase options |

Avail of customized purchase options to meet your exact research needs. |

This report forecasts revenue growth at country levels and provides an analysis of the latest industry trends in each of the sub-segments from 2014 to 2025. For the purpose of this study, Million Insights has segmented the U.S. automotive collision repair market report based on product type, vehicle type, and service channel:

• Product Type Outlook (Revenue, USD Billion, 2014 - 2025)

• Paints & Coatings

• Consumables

• Spare Parts

• Vehicle Type Outlook (Revenue, USD Billion, 2014 - 2025)

• Light-duty vehicles

• Heavy-duty vehicles

• Service Channel Outlook (Revenue, USD Billion, 2014 - 2025)

• DIY (Do it Yourself)

• DIFM (Do it for Me)

• OE (Handled by OEMs)

Research Support Specialist, USA